Kotak Assured Income Plan

is a traditional savings cum protection plan with 15 years premium paying term

and provides protection for 30 years. The highlight of the plan is guaranteed tax

free annual income for 20 years to the policyholder from the 10th

policy year until the maturity i.e. for a period of 20 years. The plan also

pays, apart from the guaranteed annual income, a lumpsum amount of maturity

that will be 104-110% of the basic sum assured. The plan also offers rides for

extra protection and loan facility.

Let’s have a look on what

you pay and what you get. The returns are based on a 30 year old healthy person:

Annual

Premium

|

Life

Cover/

Death

Benefit

|

Total

Premium Payable During Policy Term

|

Guaranteed

Income

|

Total

Guaranteed Income Received

|

Lump-sum

receipt on Maturity

|

Total

Returns From Kotak Assured Income

|

10 Times The Annual

Premium

|

Premium Paying Term is

15 Years

|

From 10th

Till 30th Policy Year

|

Cumulated for 20 Years

|

107% of Sum Assured

|

After 30 years

|

|

10,000

|

1,00,000

|

1,50,000

|

9,100

|

1,82,000

|

1,07,000

|

2,89,000

|

25,000

|

2,50,000

|

3,75,000

|

24,000

|

4,80,000

|

2,67,500

|

7,47,500

|

50,000

|

5,00,000

|

7,50,000

|

48,000

|

9,60,000

|

5,35,000

|

14,95,000

|

75,000

|

7,50,000

|

11,25,000

|

75,000

|

15,15,000

|

8,02,500

|

23,17,500

|

1,00,000

|

10,00,000

|

15,00,000

|

1,01000

|

20,20,000

|

10,70,000

|

30,90,000

|

Let’s go through the

features now:

1. Guaranteed Returns:

As mentioned early, the

major highlight of this plan is the guaranteed or assured annual returns for 20

years from the 10th policy year. The annual tax free guaranteed

percentage returns depend upon the premium that you pay. The assured returns

range from 9.10% to 10.10% per annum of the sum assured.

Premium Bands

|

Assured

Annual Income

|

Up to Rs. 24,999

|

9.10%

|

Rs. 25,000 to Rs. 74,999

|

9.60%

|

Rs. 75,000 and above

|

10.10%

|

2. Premium Payment

Period:

The premiums are to be paid for the

period of 15 years.

3. Life Cover:

The plan offers you the sum assured 10

times of the annual premium for 30 years. In case of death of policyholder

during the policy term, the nominee/beneficiary will get the basic sum assured.

4. Maturity:

The plan matures after 30 years. So in

addition to giving a assured income for 20 years, the plan gives you a lumpsum

equal to 104% to 110% of Basic Sum Assured on maturity.

5. Riders:

The plan gives you the following riders

for additional protection:

v Kotak

Accidental Death Benefit (ADB)

v Kotak

Permanent Disability Benefit (PDB)

v Kotak

Life Guardian Benefit (LGB)

v

Kotak Accidental Disability Guardian Benefit

(ADGB)

6. Eligibility:

v

Age at entry: 0 to 60 years

v

Age at maturity: 30 to 90 years

v Minimum & Maximum Premium: The minimum is Rs. 10,000 per

annum and has no maximum limit. However the maximum amount always depends upon

the financial and insurance writing norms.

7. Loan Facility:

After the policy

completes 3 years, you can avail a loan against your policy. The maximum loan

can be up to 80% of the surrender value and the rate of interest will be

declared by the company from time to time. The minimum loan amount is Rs.

10,000.

8. Surrender Value:

The policy acquires

guaranteed surrender value of 30% of the premiums paid after 3 years. However

it excludes the first premium and the rider premiums.

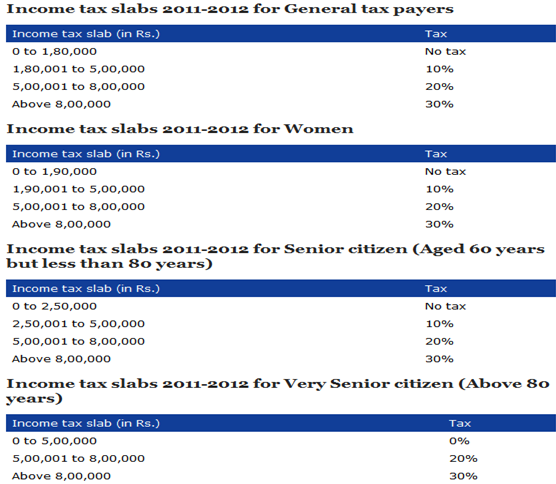

9. Tax Benefits:

The premiums paid are

eligible for tax deduction under section 80C and the annual guaranteed income will

be tax free as per current tax laws.

Should You Take This Plan?

The people who seek the

capital protection with guaranteed returns year after year may go for it. So if

you would rather prefer the guaranteed returns with peace of mind and are not

comfortable with the uncertainties and high risk market linked products where

the returns are tied to market performance, then go for it. Among the traditional

investment products on offer by insurance companies, this is certainly the

excellent plan. However if you need a bigger life cover, check term plans.