Tax Planning For FY 2011-12 Where To Invest & Save Tax ?

The current financial year is going to be completed on 31st March, 2012. Everybody will be in planning How to Save Income Tax? Here we will discuss all about Tax Planning. We should pay taxes every year as responsible citizens. However, the law allows certain “tax-deductible” savings and we owe it to ourselves to benefit from these options, which could translate into future savings. Every citizen has a fundamental duty to pay taxes honestly and a fundamental right to avail of all the tax incentives that the law provides. Therefore, through prudent tax planning, not only can we reduce our income-tax liability but also secure our future through compulsory savings. Let us see how one can do successful tax planning to enjoy optimum benefits.

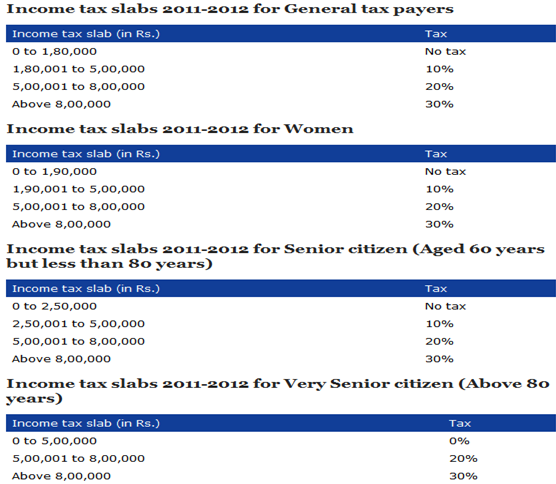

Know The Tax Slabs/brackets:

The Most Important Section For Individual Tax Payers For Tax Saving – Section 80C

In order to encourage savings, the government gives tax breaks on certain financial products under Section 80C of the Income Tax Act. Under this section, you can invest a maximum of Rs 1 lakh and if you are in the highest tax bracket of 30%, you save a tax of Rs 30,000.

Qualifying Investment options under Section 80C

Investment options with Section 80C can be segregated as follows:

Provident Fund & Voluntary Provident Fund: Provident Fund is deducted directly from your salary by your employer. The deducted amount goes into a retirement account along with your employer’s contribution. While employer’s contribution is exempt from tax, your contribution (i.e., employee’s contribution) is counted towards section 80C investments. You can also contribute additional amount through voluntary contributions (VPF).

Provident Fund & Voluntary Provident Fund: Provident Fund is deducted directly from your salary by your employer. The deducted amount goes into a retirement account along with your employer’s contribution. While employer’s contribution is exempt from tax, your contribution (i.e., employee’s contribution) is counted towards section 80C investments. You can also contribute additional amount through voluntary contributions (VPF).

Public Provident Fund: An account can be opened with a nationalized bank or Post office. The current rate of interest is 8%, which is tax-free and the maturity period is 15 years. The minimum amount of contribution is Rs 500 and the maximum is Rs 10,00,00.

National Savings Certificate: These are now 5-year small-savings instrument, where the rate of interest is 8% and is compounded half-yearly. The interest accrued every year is liable to tax but the interest is also deemed to be reinvested and thus eligible for section 80C deduction.

Life Insurance Premiums: Any amount that you pay towards life insurance premium for yourself, your spouse or your children can be included in section 80C deduction. If you are paying premium for more than one insurance policy, all the premiums can be included. Besides this, investments in unit-linked insurance plans (ULIPs) that offer life insurance with benefits of equity investments are also eligible for deduction under Section 80C. The things are however going to change after the introduction and implementation of DTC. So be careful if you are buying new insurance policies just to save tax. You may be in for shock later on. So better consult your financial planner (not insurance agent).

Equity-linked savings scheme (ELSS): An ELSS (equity-linked savings scheme), offered by mutual funds, is a diversified equity scheme with a three-year lock-in period, providing tax benefits under Section 80C of the IT Act. As 80-100% of the corpus in a diversified equity scheme is invested in the equity market, the performance of these funds is in line with market trends.

Tax benefits for ELSS, however, will become history once the new DTC comes into force on April1, 2012. So this year is probably is the last opportunity for anyone looking to save tax through ELSS.

Home Loan Principal Repayment: Your EMI consists of two components, namely principal and interest. The principal component of the EMI qualifies for deduction under Section 80C. Even the interest component can save you significant income tax – but that would be under Section 24 of the Income Tax Act.

Home Loan Principal Repayment: Your EMI consists of two components, namely principal and interest. The principal component of the EMI qualifies for deduction under Section 80C. Even the interest component can save you significant income tax – but that would be under Section 24 of the Income Tax Act.

Stamp Duty and Registration Charges For Home: The amount you pay as stamp duty when you buy a house, and the amount you pay for the registration of the documents of the house can be claimed as deduction under section 80C. However, this can be done only in the year in the year of purchase of the house.

Five-Year Bank fixed deposits: Tax-saving fixed deposits (FDs) of scheduled banks with tenure of five years are also entitled for section 80C deduction.

Children’s Tuition Fees: Apart from the above, things like children’s tuition fees expenses that can be claimed as deductions under Section 80C. However, you need receipts to claim the same.

Senior Citizen Savings Scheme 2004 (SCSS): A recent addition to section 80C list, Senior Citizen Savings Scheme (SCSS) is the most lucrative scheme among all the small savings schemes but is meant only for senior citizens. Current rate of interest is 9% per annum payable quarterly. Please note that the interest is payable quarterly instead of compounded quarterly. Thus, unclaimed interest on these deposits won’t earn any further interest. Interest income is chargeable to tax.

5-Yr post office time deposit (POTD) scheme: POTDs are similar to bank fixed deposits. Although available for varying time duration like one year, two year, three year and five year, only 5-Yr post-office time deposit (POTD) – which currently offers 7.5 per cent rate of interest –qualifies for tax saving under section 80C. Effective rate works out to be 7.71% per annum (p.a.) as the rate of interest is compounded quarterly but paid annually. The Interest is entirely taxable.

No comments:

Post a Comment